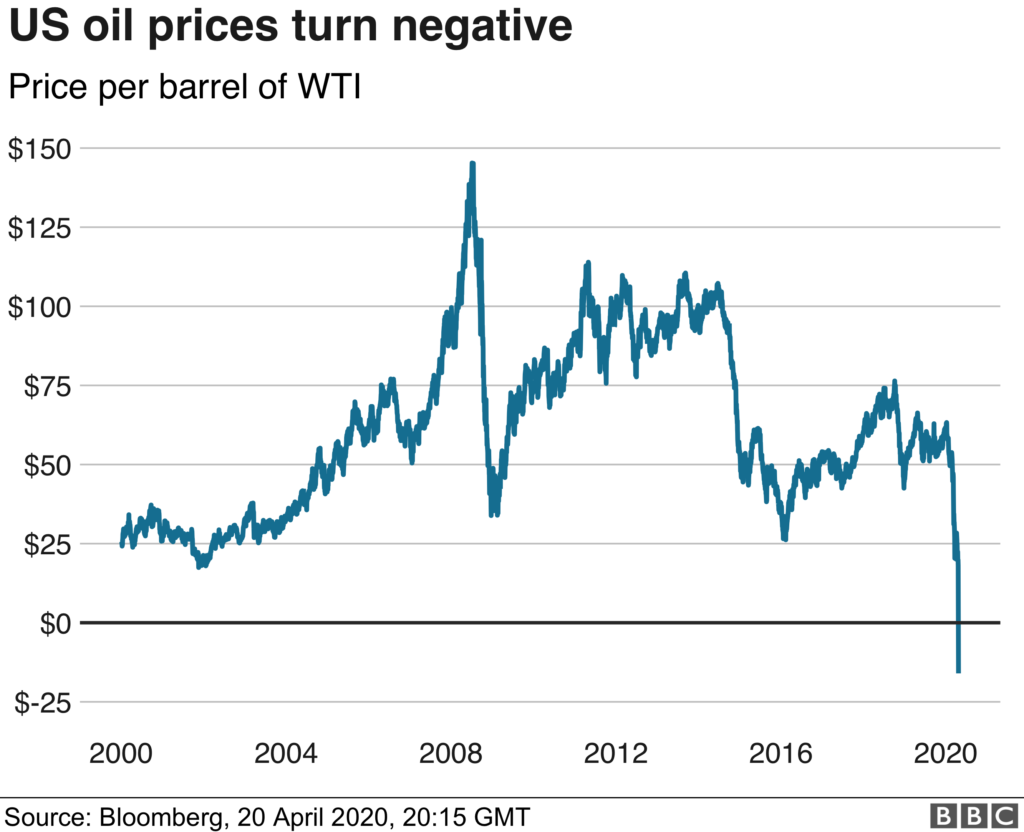

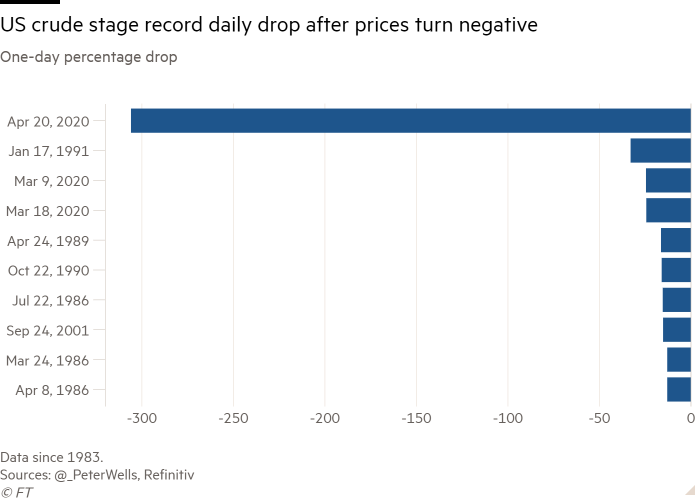

US oil prices turned negative for the first time in history on Monday amid the deepest fall in demand in 25 years. A flood of unwanted oil in the market caused the West Texas Intermediate (WTI), the benchmark price for US oil, to plummet to almost –$40 a barrel after the fastest plunge in history. That means oil producers are paying buyers to take the commodity off their hands over fears that storage capacity could run out in May.

Demand for oil has all but dried up as lockdowns across the world have kept people inside. As a result, oil firms have resorted to renting tankers to store the surplus supply and that has forced the price of US oil into negative territory.

The price of a barrel of West Texas Intermediate (WTI), the benchmark for US oil, fell as low as minus $37.63 a barrel.

“This is off-the-charts wacky,” said Stewart Glickman, an energy equity analyst at CFRA Research. “The demand shock was so massive that it’s overwhelmed anything that people could have expected.”

The severe drop on Monday was driven in part by a technicality of the global oil market. Oil is traded on its future price and May futures contracts are due to expire on Tuesday. Traders were keen to offload those holdings to avoid having to take delivery of the oil and incur storage costs.

June prices for WTI were also down, but trading at above $20 per barrel. Meanwhile, Brent Crude – the benchmark used by Europe and the rest of the world, which is already trading based on June contracts – was also weaker, down 8.9% at less than $26 a barrel.

Mr Glickman said the historic reversal in pricing was a reminder of the strains facing the oil market and warned that June prices could also fall, if lockdowns remain in place. “I’m really not optimistic about the prospects for oil companies or oil prices,” he said.

US President Donald Trump has said the government will buy oil for the country’s national reserve. But concern continues to mount that storage facilities in the US will run out of capacity, with stockpiles at Cushing, the main delivery point in the US for oil, rising almost 50% since the start of March, according to ANZ Bank.

Dealers speculated that traders who had successfully leased storage were putting pressure on rivals without access to tank farms. That could allow them to snap up ultra-cheap oil for their storage tanks, before locking in much higher prices in the futures market, essentially being paid to take oil and then selling it a month later for more than $20.

Traders said contracts for later delivery were being propped up by hopes the worst of the demand destruction could be passed by the summer, if lockdowns and travel bans are eased. But others are questioning whether the record-breaking gaps between cash trades and contracts for later delivery are sustainable.

Summary

1. Why have US oil prices turned negative?

The price of oil has been steadily falling across global markets since coronavirus first broke out in China at the end of 2019. Since then, the shutdown of major economies and travel routes to curb the spread of the virus has wiped out oil demand as transport has ground to a halt. But oil producers have continued to pump crude from their wells, causing a catastrophic imbalance between oversupplied oil and the biggest slump in demand for 25 years.

2. What do ‘negative prices’ mean?

In short: oil producers are paying buyers to take the barrels of oil off their hands because storage facilities are full to the brim. At the market’s lowest point on Monday, an oil company might have paid about $40 for every barrel of oil someone was willing to take. A buyer would need to factor in the cost of transporting oil from the well to a shipping port, or a storage facility, where it may need to be held for up to six months, at significant cost. They would also need to bet that oil prices will rise later this year to make a return on the “investment”. No oil company wants to “sell” their crude at a loss, so many producers are likely to shut their wells until the market recovers.

3. Why are oil prices in other countries still above zero?

The world’s oversupply of oil is particularly acute in the US, which produces around 10m barrels of oil every day, because oil storage tanks have filled up, leaving oil companies desperate to sell their surplus barrels. In other regions, including the UK, oil prices are still above zero in part because they face lower transport costs and easier access to ports. Still, no oil market has remained unscathed. The international benchmark oil price, known as Brent crude, is still above $20 a barrel, but has fallen by two-thirds since January to 18-year lows.

4. What does this mean for petrol prices?

Petrol prices are likely to fall sharply this year due to the sudden collapse of oil prices and the long road to market recovery that probably lies ahead. But it is worth keeping in mind that the price paid at the pump is not a perfect reflection of the oil markets because petrol and diesel prices include government taxes and a profit margin for the seller. The negative oil prices seen in the US will be short-lived, so no one should expect to be paid for filling up their car.

5. Are prices likely to recover?

Yes, and quite quickly. The negative US oil price referred specifically to the price for crude delivered in May, the month in which oil demand is expected to be lowest and supplies are expected to be highest. From Tuesday, oil traders will begin trading barrels for delivery in June in earnest, and these are expected to fetch far higher prices. A meaningful recovery of oil market prices will depend on how quickly demand for transport fuels increases – a speedy end to lockdown would accelerate a market price recovery, but a slow emergence from the Covid-19 crisis could mean further financial pain for oil producers until 2021.

Read other related news:

- UN chief Guterres salutes countries like India for helping to fight against coronavirus

- $20 trillion lawsuit filed against China over COVID-19

Views : 73589